Unpaid invoices are one of the fastest ways a small business cash flow can fall apart. In 2025, late payments still hit UK SMEs hard—FSB reports that thousands face cash strain every month because customers ignore credit terms or delay payments without warning.

If you’re searching for small business debt recovery, you’re likely dealing with the same frustration: chasing money that should already be in your account. This guide breaks down what actually works today—step-by-step, legally compliant, simple enough to follow without a law degree.

You’ll get a clear recovery process, practical examples, templates you can replicate, and when to escalate to an agency or small claims court. This isn’t a generic overview—it’s built for real small business owners who need clarity, not jargon.

What Is Small Business Debt Recovery?

Small business debt recovery is the process of collecting money owed to your business when a customer fails to pay an invoice by the agreed date. In the UK, you have legal rights to charge:

-

Statutory interest (8% + Bank of England base rate)

-

Debt recovery fees (£40–£100 depending on invoice size)

These rules fall under the Late Payment of Commercial Debts Act.

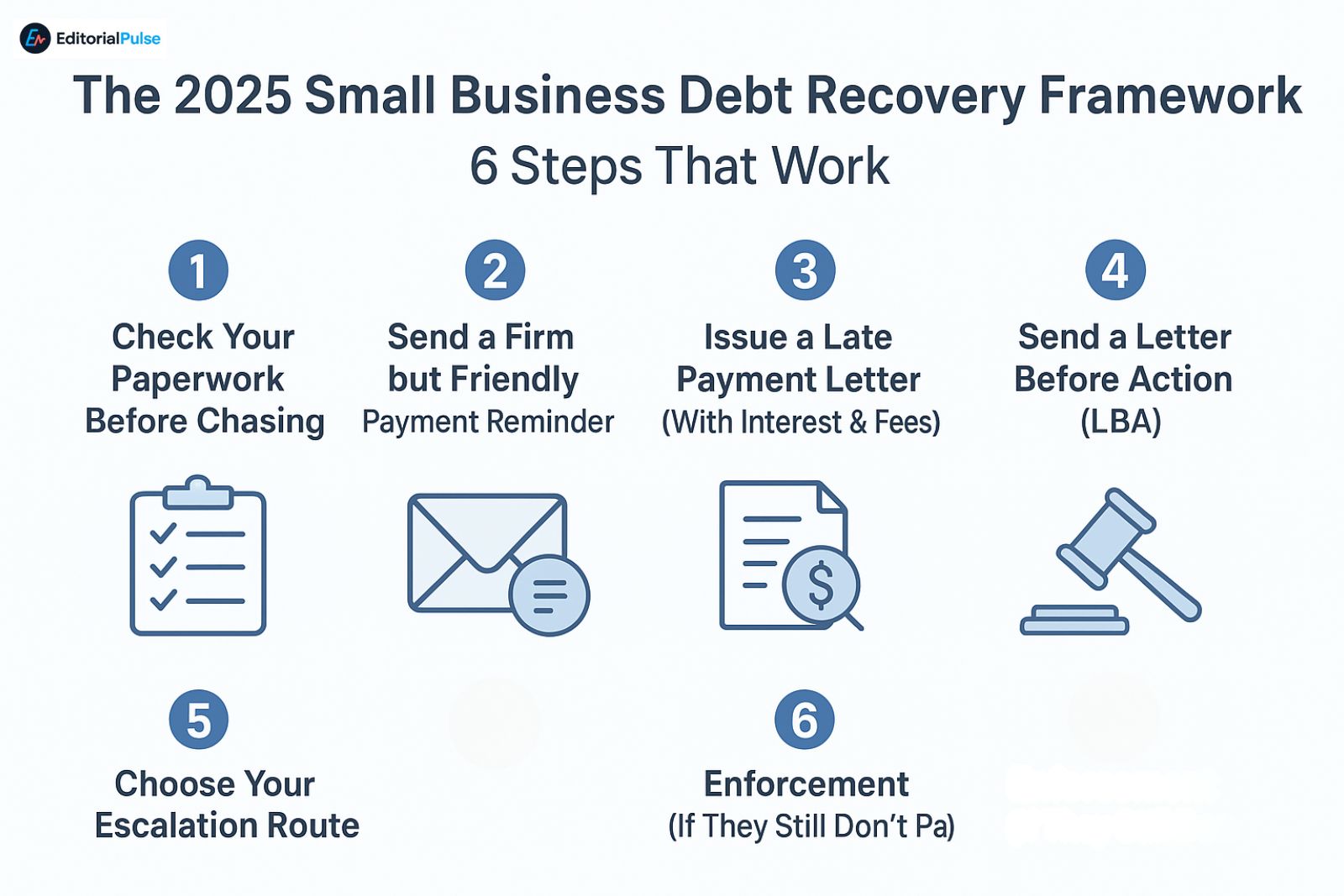

The 2025 Small Business Debt Recovery Framework (6 Steps That Work)

This is the unique system your article offers — a clear, replicable process.

Step 1 — Check Your Paperwork Before Chasing

Before sending any recovery messages, confirm:

-

Invoice is correct

-

PO numbers match

-

Goods/services were delivered

-

Any credit terms or email agreements are documented

Why it matters:

Over 30% of disputes come from simple admin errors.

Step 2 — Send a Firm but Friendly Payment Reminder

People often pay after one clear reminder.

Keep it short:

Example:

“Hi [Name], invoice #1043 dated [date] was due on [date]. Could you confirm payment status today?”

Avoid long explanations—they reduce response rate.

Step 3 — Issue a Late Payment Letter (With Interest & Fees)

If the reminder fails, use the legal protections available.

Under UK law (commercial debts):

-

Statutory interest = 8% + BoE base rate

-

Recovery fee:

-

£40 for debts up to £999

-

£70 for £1,000–£9,999

-

£100 for £10,000+

-

2025 example calculation:

Invoice: £4,000

Interest: (8% + 5.25% base rate) = 13.25% yearly

Daily rate ≈ £1.45/day

This shows customers you understand your rights.

Step 4 — Send a Letter Before Action (LBA)

This is the letter courts expect before you claim.

Include:

-

Amount owed

-

Interest + fees

-

Deadline (usually 7–14 days)

-

Statement of intent to issue court proceedings

Most UK service providers (Thomas Higgins, etc.) offer fixed-fee LBAs because they work.

Step 5 — Choose Your Escalation Route

You have three realistic options.

Option A: DIY → Money Claim Online (MCOL)

Works best for debts under £10k.

Option B: Debt Collection Agency

Good when you prefer:

-

No win, no fee

-

Faster recovery

-

Avoiding court admin

Option C: Solicitor-Led Recovery

Best if:

-

Debtor disputes the invoice

-

The claim is £10k+

-

You need a County Court Judgment (CCJ)

-

You expect enforcement

Step 6 — Enforcement (If They Still Don’t Pay)

If the court rules in your favour, you may use:

-

High Court Enforcement Officers (HCEOs)

-

Attachment of earnings

-

Charging orders

-

Third-party debt orders

Most small businesses only reach this step for higher-value debts.

DIY vs Agency vs Solicitor: What’s Best for Small Businesses?

| Option | Best For | Cost | Pros | Cons |

|---|---|---|---|---|

| DIY / MCOL | Small, straightforward debts | Low fees | Low cost, simple online system | Time-consuming, no negotiation |

| Debt Collection Agency | Busy owners, older debts | Commission or % | Fast, persistent, no court work | Not ideal for disputes |

| Solicitor | High-value, disputed cases | Fixed fees or hourly | Strong legal pressure, court-ready | Pricier upfront |

Real Small Business Case Study (Mini Example)

Business: IT consultant (1-person company)

Debt: £3,200 outstanding for 67 days

Steps taken:

-

Friendly reminder → ignored

-

Late payment letter with interest → no reply

-

LBA sent → client responded but stalled

-

MCOL claim issued

-

Payment + fees + interest paid on day 12

Total recovered: £3,368

This shows the process works when followed methodically.

Common Mistakes Small Businesses Make (Avoid These)

-

Waiting 60–90 days before acting

-

Not adding interest (loses leverage)

-

Not keeping delivery records

-

Accepting “promises to pay” repeatedly

-

Unclear payment terms

-

Sending emotional or overly long messages

Small Business Debt Prevention Checklist (2025)

-

Clear credit terms on every invoice

-

Automated payment reminders

-

Deposit or milestone payments for larger projects

-

Upfront credit checks

-

Signed contracts or email confirmation

-

Shorter payment terms (7–14 days for SMEs)

FAQs

Q. What is the 7-7-7 rule for collections?

It’s a reminder rule used by some agencies: follow up at 7 days overdue, 14 days overdue, and 21 days overdue. It’s not a legal requirement—just a structured chase pattern.

Q. Which debts cannot be recovered?

Debts that are time-barred (usually after six years), disputed contracts without proof of delivery, or debts where the debtor is insolvent and has no assets.

Q. Are small business owners personally liable for company debts?

In a limited company, directors aren’t personally liable unless they provided a personal guarantee or acted wrongfully.

Q. How long should I chase before taking legal action?

Typically 14–28 days after an LBA. Waiting too long weakens your claim and delays cash flow.

Q. Is no win, no fee debt recovery worth it?

It can be. It removes upfront risk, but agencies charge a percentage, so it works best for older or lower-value debts.

Conclusion

Small business debt recovery doesn’t have to be overwhelming. When you apply a clear process—reminders, interest letters, LBAs, and escalation options—you take control instead of reacting late. The goal is simple: recover payment fast, without harming your business.

Use this guide as your 2025 roadmap to protect cash flow and keep overdue invoices from turning into long-term debt.

For more insights and related guides, visit our website: EditorialPulse

| This article provides general guidance on small business debt recovery in the UK as of 2025. It is for informational purposes only and does not constitute legal advice. For advice specific to your situation, including legal or financial actions, consult a qualified solicitor or debt recovery professional. We are not responsible for any losses arising from actions taken based on this content. |