Getting a car loan with bad credit can feel like trying to clear a hurdle while spinning. If you’re searching for car loans for bad credit, you’re not alone — in fact, many lenders are still willing to finance vehicles even when your credit history isn’t perfect. The key: knowing what to expect, how to strengthen your position and how to shop smart. In this guide we’ll cover everything you need — from how lenders evaluate your application, to real lender comparison data, to a step‑by‑step preparation checklist — all updated for 2025. You’ll leave with a plan, not just hope.

Why It’s Harder to Get a Car Loan with Bad Credit

What “bad credit” means

“Bad credit” typically means your credit score is lower than the threshold many prime lenders use (often 620‑650 in the U.S.). It could also mean you’ve had recent missed payments, bankruptcy or little credit history.

How lenders view risk

When your credit is weak, lenders see you as a higher risk. That usually means:

- Higher interest rates (to compensate risk)

- Larger down‑payment requirements

- Shorter loan terms

- More strict documentation or co‑signer requirement

For example, according to one study, borrowers with “bad credit” might face APRs in the double‑digits — significantly above what prime borrowers pay.

The current environment (2025)

In 2025, the market is even more cautious. For example:

- A recent Reuters article notes sub‑prime auto loan delinquencies (borrowers 60 days+ behind) reached 6.65% in October 2025 — the highest since the early 1990s.

- Because new‑car prices are more than ever (over US$50,000 average), lenders are pushing longer terms and higher risk portfolios.

Takeaway: If you have bad credit and you’re seeking a car loan, you must be extra prepared — the risk environment is tougher.

What You (the Borrower) Can Do to Improve Your Chances

Step‑by‑step system

Here’s a proven preparation system:

- Check your credit report & score — Obtain your credit report, look for errors (missed payments, collections) and correct them.

- Gather documentation — Stable income (pay slips, bank statements), proof of address, proof of employment. Some lenders will look beyond credit score and weigh income/debt ratio.

- Save for a down payment — The more you can put down, the lower your risk to the lender.

- Choose an affordable car — Loan size = vehicle price + interest. Avoid going for “dream car” if it pushes your payment too high.

- Select shorter loan term if possible — Longer terms reduce monthly payment but increase total cost and risk of being “upside down” (owing more than car value).

- Pre‑qualify with multiple lenders — That gives you rate options without full impact to credit (soft check).

- Avoid “Buy Here Pay Here” unless last resort — These often have very high rates and less favourable terms; only consider if no other option.

- Build your credit while repaying — Once you have the car and the loan, paying on time helps rebuild your credit for future borrowing.

What to avoid (common mistakes)

- Thinking you’ll always get “low‑rate” just because you applied. With bad credit, your rate will likely be higher — so focus on service and transparency.

- Accepting a loan that pushes your monthly payments uncomfortably high. If you miss payments, it will wreck your credit further.

- Skipping fine print: some bad‑credit loans have hidden fees, balloon payments or restrictive clauses.

- Fixating only on the monthly payment — total cost (APR × loan term) matters. A low monthly payment over 84 months can cost way more interest.

How to Compare Your Options – Lender Table

Here’s a comparison of real lenders and what you might expect in 2025 when your credit isn’t great.

| Lender | Minimum Credit / Accepts | APR / Rate Range | Strengths for Bad Credit | Potential Drawbacks |

| Auto Credit Express | Very low / no set minimum (even bankruptcy) | Varies (depends on sub‑finance dealer) | Specialist network for bad credit borrowers | Rates may be very high; down payment likely |

| Capital One Auto Finance | Subprime accepted (~500 score) | From ~5% for more qualified; higher for bad credit | Pre‑qualification available; large dealer network | High APR for low score; dealer‑only financing |

| Carvana | No explicit minimum credit score | ~6.85%–16.5% depending on credit (used vehicle) | One‑stop online financing + car purchase | Higher rates; limited to inventory; used car only |

| RoadLoans (Santander Consumer USA) | Subprime borrowers | ~9%–25% depending on risk profile | Direct‑to‑consumer; strong subprime infrastructure | Very high APR; more interest paid over time |

| Credit Acceptance Corporation | Very bad credit / high risk | Often 15%–30%+ for subprime | Accepts very low‑credit borrowers; rebuild path | Extremely high cost; large down payments; risk of debt trap |

| Credit Unions (various) | Varies; more flexible | Possibly 6%–14% for lower‑credit borrowers | Lower cost; better customer service; potential for co‑signer | Membership needed; may still require proof and decent income |

How to use this table:

- Use the “Strengths” and “Drawbacks” to filter what matters for you.

- Always check the APR you’ve been quoted against credit‑score range.

- Focus on lenders that accept lower credit but also show transparency in rates and terms.

- Review total cost (monthly × term) not just monthly payment.

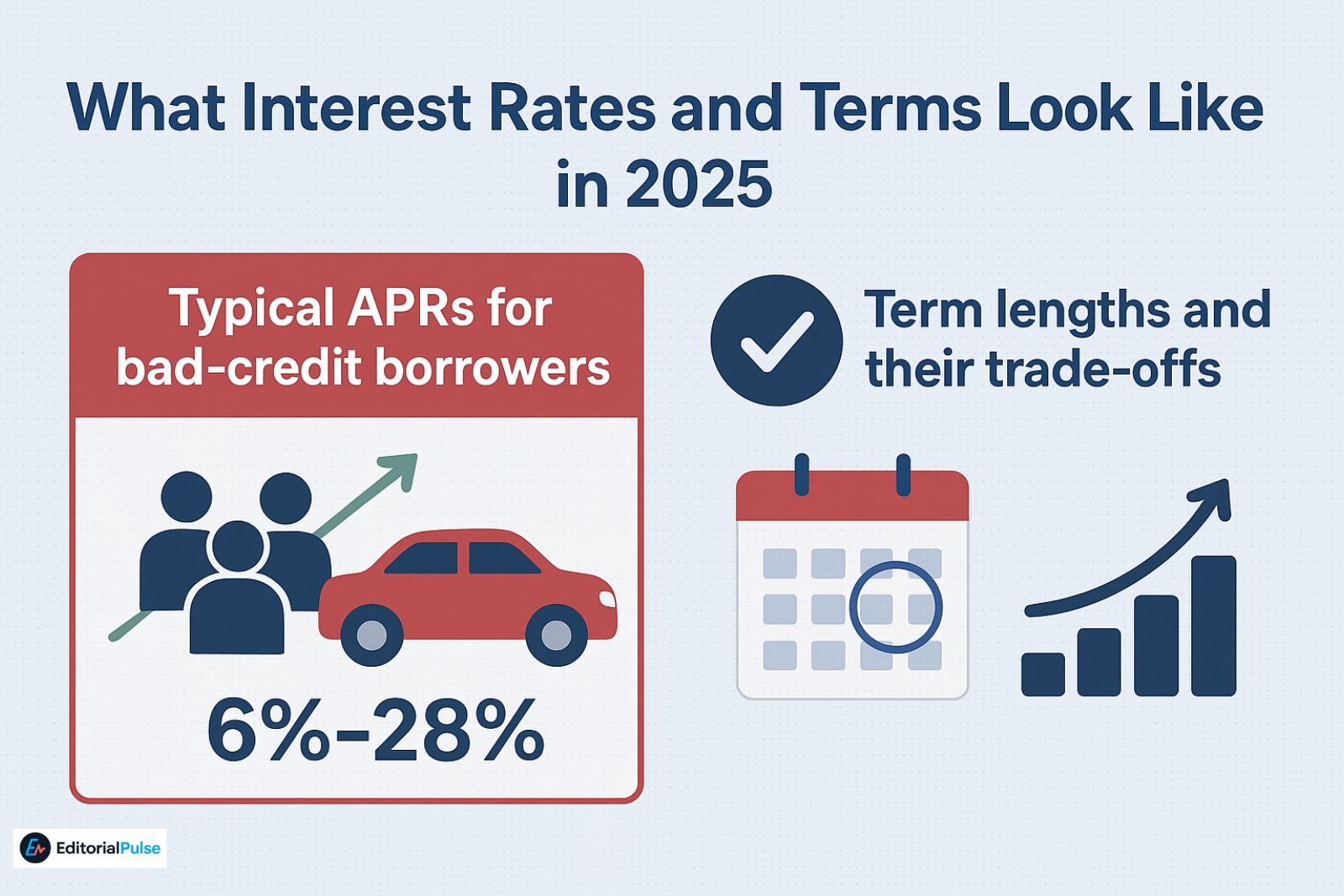

What Interest Rates and Terms Look Like in 2025

Typical APRs for bad‑credit borrowers

According to recent data:

- One review shows minimum recommended credit score 580 for one aggregator, with APR range for used vehicles of ~6%–28%.

- Another guide notes lenders charge higher rates for bad credit; affordable income and debt‑to‑income ratio matter more than just score.

Term lengths and their trade‑offs

- Longer terms reduce monthly payments but increase total interest and increase risk of owing more than the car’s value.

- A recent article cites that many buyers are taking 7‑year+ vehicle loans in 2025, which raises risk especially for subprime borrowers.

Takeaway: If your credit is poor, expect the APR and/or term to be higher/worse. Your goal is: secure the best term you can while keeping payment manageable.

Used Car Loans for Bad Credit – What to Consider

Since used vehicles often cost less, they’re common for bad‑credit borrowers. But there are pitfalls.

Pros

- Lower vehicle cost → smaller loan required

- Easier to find financing at lower amounts

- Potentially lower monthly payment

Cons

- Older cars may have higher maintenance, which adds cost

- Some lenders restrict used vehicle age/mileage for bad‑credit borrowers

- If the car devalues quickly, you risk being “upside down” (owing more than car is worth)

Best practices for used car loan

- Choose a reliable model with good maintenance history

- Aim for a down payment (10‑20% if possible)

- Keep term moderate (e.g., 36‑60 months) not 84+ months

- Verify lender’s used‑car policy (age, mileage limits)

Mistakes to Avoid When Taking a Car Loan with Bad Credit

- Accepting the first offer without comparison

- Focusing only on monthly payment — total cost matters

- Taking the longest term just because payment is low

- Not reading the fine print: fees, balloon payments, pre‑payment penalties

- Using the car as “credit repair” without realistic payment ability — missing payments will damage credit further

Future Trends & What to Watch (2025‑Beyond)

- Rising subprime delinquencies: More borrowers with bad credit are falling behind, which may tighten future lending options.

- Higher new car prices: With average new car price above US$50k, even used‑car buyers feel pressure on budgets.

- More fintech/alternative‑lending models: Some lenders now consider alternative data (income stability, bank statements) in addition to credit scores.

- Regulatory scrutiny: As subprime auto lending grows risk‑wise, watchdogs may impose stricter rules or disclosures (especially for high‑cost loans).

FAQs

Q1: Can you get approved for a car loan with a 500 credit score?

Yes — some lenders will approve borrowers with credit scores around 500 or even lower, especially if there’s stable income, a down payment, or a co‑signer. But expect higher interest rates and stricter terms.

Q2: What is the lowest credit score for a car loan?

There’s no single minimum that applies everywhere. Some lenders accept scores near 500; others may require 550‑600. Beyond credit score, lenders also look at income, debt ratio and vehicle specifics.

Q3: What interest rate can I expect for a car loan with bad credit?

For bad‑credit borrowers in 2025, APRs may fall into the double‑digits (for example 9%‑25% or more) depending on credit, income, down payment and loan term.

Q4: What are the easiest car loans to get with bad credit?

“Easiest” usually means lenders that specialise in subprime financing, or dealer‑finance models. But “easy” doesn’t mean cheap. Always examine total cost, not just approval.

Q5: Is refinancing a car loan bad for your credit?

Refinancing itself isn’t inherently bad — if you do it correctly (no late payments, lower APR, shorter term) it could improve your credit. But if you extend the term much longer, it might cost you more, and extra hard inquiries can affect your score.

Q6: Should I buy a used car if I have bad credit?

Buying a used car can be smart because loan size is smaller and you may find more flexible financing. But you must factor in maintenance cost, ensure the vehicle is reliable, and avoid overly long loan terms.

Q7: How soon after repairing my credit can I get a good car loan?

It depends, but typically when you’ve shown 6‑12 months of on‑time payments, reduced debt load and stable income, lenders will view you more favorably. Some lenders accept borrowers with a 6‑month credit history.

Q8: What down payment should I aim for with bad credit?

The more the better — ideally 10‑20% of the vehicle cost — because it lowers risk for the lender and improves your chances of better terms. Some lenders may require higher down payments when credit is weak.

Conclusion

If you’re searching for car loans for bad credit, here are the key take‑aways:

- Yes, you can get a car loan — but expect higher cost and prepare accordingly.

- Your best move is to strengthen your profile: document income, save a down payment, choose a car you can afford and compare lenders.

- Use the comparison table above to identify lenders geared to your credit level, and read all terms.

- Avoid the trap of “cheap monthly payment but large total cost”.

- Once you have the car and loan, make every payment on time — this is a chance to rebuild your credit for the future.

You’re in control of how you approach this. With preparation and care, you can drive away in a reliable vehicle and rebuild your financial standing — even with bad credit.

For more insights and related guides, visit our website: EditorialPulse